Firm Statistics of Manufacturing Sector in Kazakhstan

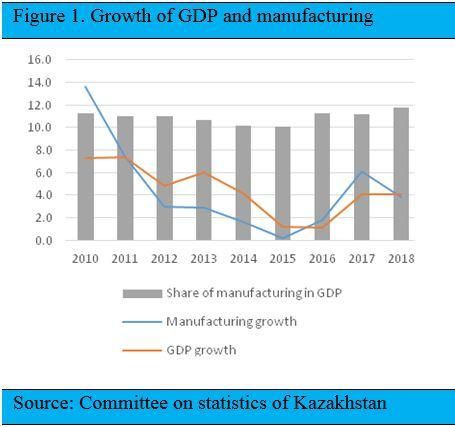

On May 14, 2019, during the governmental meeting, Kazakhstan’s Cabinet of Ministers and regional governors presented their reports to Prime Minister Askar Mamin summarizing the results of socio-economic development during the first quarter of 2019 (government.kz). The Prime Minister noted that in general, the country’s economy maintained a growing pattern. As it was reported by the Minister of the National Economy Ruslan Dalenov, the GDP growth during January-April reached 4% of growth compared to the same period of 2018. He also mentioned that the industrial output increased by 2.9% during January-April and noted that the growth is due to the leading pace in manufacturing, which had shown a 3.5% growth. During the first three months, this indicator was at 1.6% and was accelerated significantly by the growth in oil refining, mechanical engineering, beverage production, as well as pharmaceuticals. During the previous governmental meeting, the ministers also gave a positive evaluation to the performance of the economy and of the manufacturing industry, in particular, pointing out the 4.1% of real growth investments by 1.1 trillion tenge ($2.9 billion) (kazpravda.kz).

According to the latest data, there were 15,166 legal enterprises in manufacturing, which is around 5.2% of the total number of functioning legal entities in the economy of Kazakhstan. So there are more firms working in manufacturing than in the extractive industry, where there were only 2,830 functioning firms. Like many other industries, manufacturing is dominated by the private sector. Thus, 13,901 out of 14,861 (or 93.5%) of the functioning firms in manufacturing are firms with private ownership. If we consider the extractive sector, which is another branch of industries, this indicator is at 89.9%. If we consider the firms functioning in the economy in terms of their size, then 185,446 out of total 283,378 functioning firms (or some 65.3%) by the end of 2018 were small-sized firms with less than 100 employees.

Manufacturing has one of the highest shares of small firms, which is 84.6% whereas, in the extractive sector, this share is at 77.9%. In fact, if we derive the average size of firms in the entire economy of Kazakhstan by dividing the number of employees by the number of firms, it turns out that by the end of 2018 the average sized firm had 30.7 employees. Manufacturing had slightly larger firms with 39.1 employees per firm. On the other hand, the extractive industry on average consisted of medium-sized firms with an average size of 104.0 employees per firm.

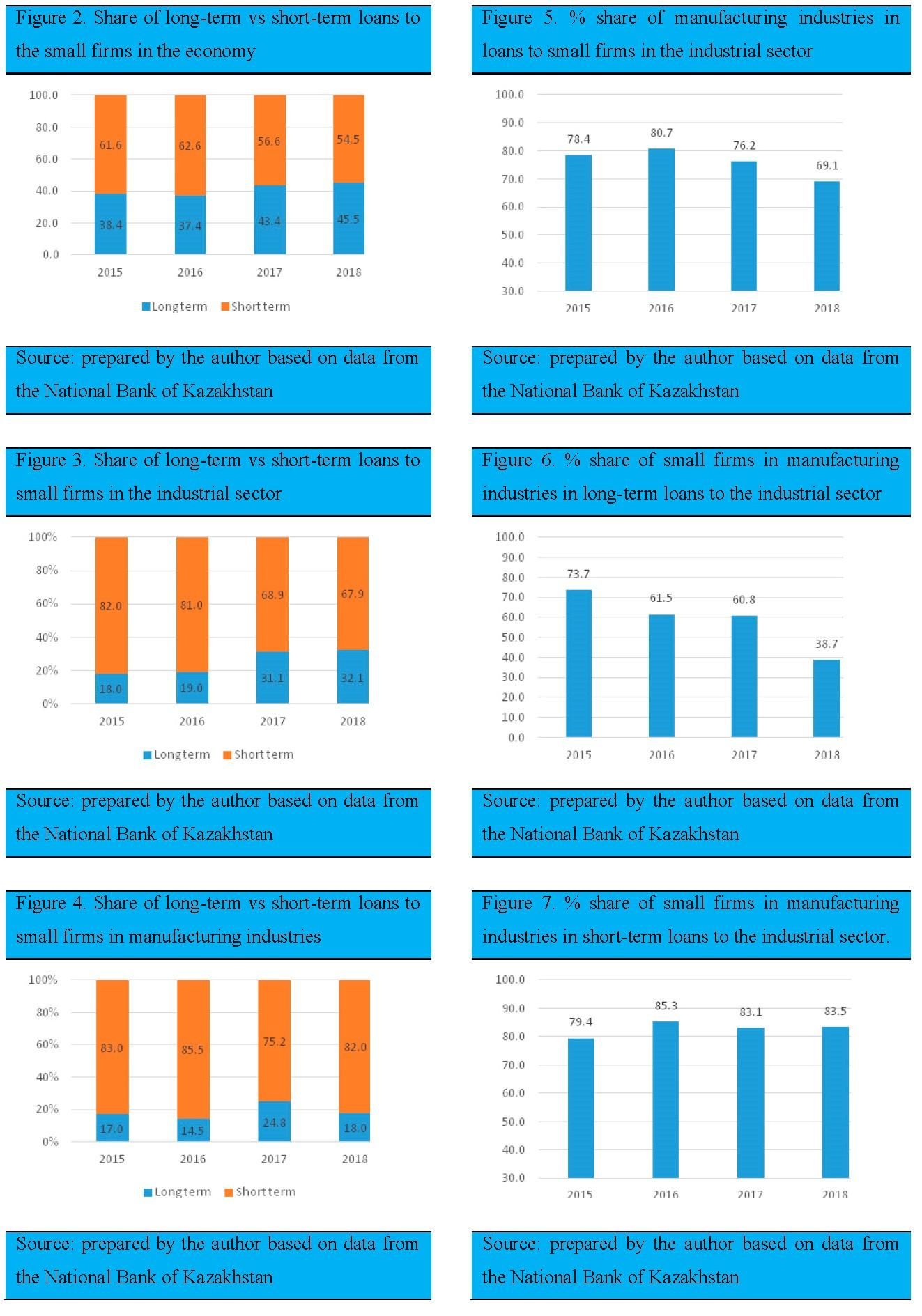

Hence, the manufacturing sector, which is the top priority sector of the economy, is basically an issue of privately owned small enterprises. In other words, addressing the problems of small private firms includes addressing the problems of manufacturing firms. One of the alternative ways of looking at the current state of firms and making projections for the near future is to look at some key financial indicators of the firms. One of such indicators is the number of loans issued by banks to firms and it is important whether the borrowings are short term or long term. It is a commonly known regularity that when firms have positive economic expectations, good financial conditions that will allow them to handle the loans they tend to take long-term borrowing from banks. Figure 2 below shows the relative shares of long-term vs short-term loans over the last four years taken by small-sized firms with less than 100 permanent employees in Kazakhstan. As we can see, there has been a small relative growth of long-term loans by small firms from 38.4% in 2015 to 45.5% in 2018. Hence, small firms are slightly better off financially and have a bit more projects for the distant future now than in 2015. Figure 3 shows the percentage share of short-term vs long-term loans by firms in the entire industrial sector, including manufacturing, extractives, utilities, etc. It turns out that the industrial sector tends to take more short-term loans than other industries. Some two-thirds of the loans issued to small firms in the industrial sector are short-term loans but the share of long-term loans have increased almost twice since 2015. Figure 4, on the other hand, shows the shares of short-term and long-term loans given by banks to small firms in manufacturing industries. As we can see, only one-fifth of the loans to small manufacturers are long-term loans and there is no tendency for the share of long-term loans to rise over the last four year. Moreover, throughout the Figures 5-7, we can see that small manufacturers not only take less and less long-term loans but also take a lesser amount of bank loans of all types.

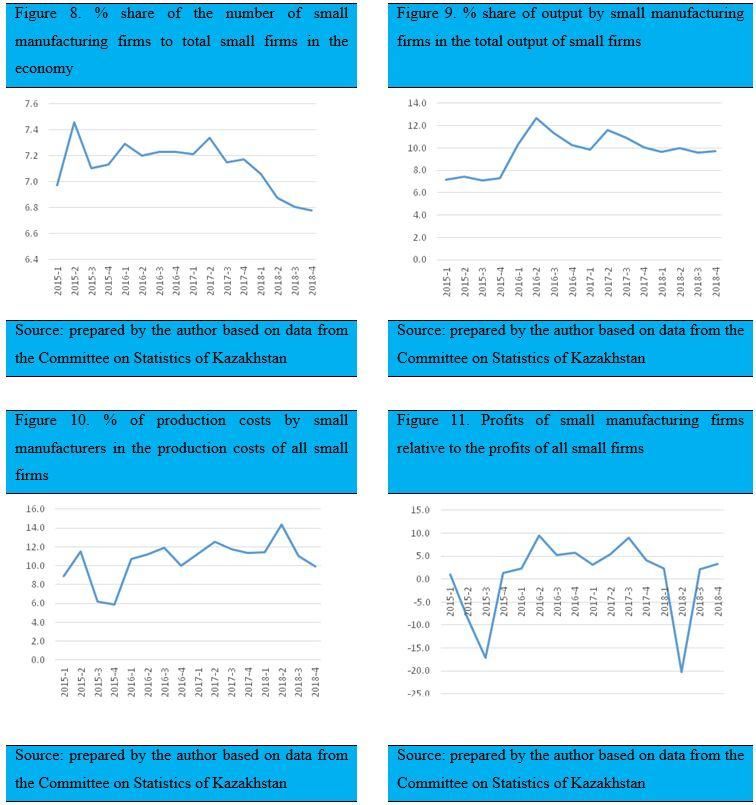

Some data from the Committee on Statistics of the Ministry of national Economy of Kazakhstan also reveals certain patterns in manufacturing industries that are not seen at first glance. Figure 8, for instance, shows that relative to all small firms operating in the economy, the number of firms in manufacturing industries decreased substantially throughout all four quarters of 2018. In fact, the number of small manufacturers decreased also in absolute terms from 12,099 to 11.912 from the fourth quarter of 2017 to the second quarter of 2018. On the other hand, the downshift of the number of firms did not affect the output of manufacturing industries, as can be seen from Figure 9. This, however, does not necessarily mean that manufacturing industries are shrinking because the number of small firms may decrease due to mergers. There has been a significant increase in the output of small manufacturing firms relative to all other small firms during the first two quarters of 2016, but since then there has been no significant change. It is also interesting to note that over time since 2015 the production costs of small manufacturing were subject to considerable fluctuations in comparison to small firms in other industries (Figure 10). But in terms of profits earned by firms, the manufacturing industries experience even larger volatility as it can be seen from Figure 11.

A general overview of data about some financial indicators of the small firms in the manufacturing industry provides some valuable information. It turns out that during 2015-2018 the relative share of long-term loans to small firms increased from 38.4% to 45.5%. The share of long-term loans by banks to small firms in the industrial sector, in general, remains significantly low, but still, there is significant growth of the relative share of long-term loans from 18.0% to 32.1%. However, we do not observe a growing share of long-term loans by small firms in manufacturing, which is not a positive sign for the industry. Moreover, not only long-term loans to small firms are decreasing but also the total amount of all types of loans to small manufacturing firms are decreasing relative to other industries. Starting from the fourth quarter of 2017 there has been also a decrease in the number of small firms operating in manufacturing in relative terms to other industries. However, this did not affect the total output produced by small manufacturing firms, which suggests that this was probably due to the transformation of small firms into medium-sized or large firms through mergers and/or acquisitions. It turns out that in comparison to other industries small firms in the manufacturing industry are subject to larger volatility in terms of production costs as well as in profits.When it comes to top priority issues of economic diversification and development of non-extractive industries and of manufacturing industries, in particular, the official reports by the ministries of Kazakhstan tend to base their conclusion on final indicators like the total output of industries, their share in the GDP, real growth rate, etc. These indicators are rather precise in describing the general situation in different industries in the economy. However, they can also be misleading in providing valuable information about important processes that determine the performance of the industries in the near future. The manufacturing industry by a very large extent (84.6%) consists of small firms with less than 100 permanent employees. The average firm size in the manufacturing sector turns out to be 39.1 employees, which is a bit larger than in the average firm size in the entire economy (30.7 employees). The extractive sector has much larger firms with an average firm size of 104 employees. However, 77.9% of the firms in the extractive sector are small firms suggesting that there are very few large firms and numerous small firms operating in the extractive industry. Hence, targeting the development of manufacturing currently in Kazakhstan is very much about targeting small firms.

The findings from some of the key microeconomic data of small firms allow us to better understand the processes going on in the manufacturing industry of Kazakhstan, disregarding some key current indicators that are often used in official reports. The main advantage of looking at some microeconomic data is that it allows us to make certain projections for the near future of the industry. Thus, the microeconomics of the small manufacturing firms in relative terms to other industries is not positive enough for us to expect major breakthroughs in the next 2-3 year. Since 2015, there has been a very sluggish growth of the manufacturing sector with very moderate growth in terms of the number of firms, employees, and output. Most importantly, there is little and diminishing demand by small manufacturers on long-term loans and on loans in general from banks suggesting that the amount of projects for the near future by small firms is very limited. We observe that small firms in manufacturing are investing less and less in production, which will have a negative effect on the overall performance of the industry. Small manufacturing firms also tend to experience large volatility in terms of production costs and profits, which makes them much vulnerable relative to small firms in other industries. Hence, significant growth of the manufacturing sector in Kazakhstan during the short-term perspectives requires additional measures supporting small firms.

References:

Committee on Statistics of the Ministry of National Economy of Kazakhstan (2019). Enterprise Finance. Retrieved from http://stat.gov.kz/faces/publicationsPage/publicationsOper/homeNumbersFinance?_afrLoop=9557711819214853#%40%3F_afrLoop%3D9557711819214853%26_adf.ctrl-state%3Du36cnfp6n_4. Accessed on 12.05.2019.

Committee on Statistics of the Ministry of National Economy of Kazakhstan (2019). Enterprise Statistics. Retrieved from http://stat.gov.kz/faces/wcnav_externalId/homeNumbersBusinessRegisters?_afrLoop=9557881376868103#%40%3F_afrLoop%3D9557881376868103%26_adf.ctrl-state%3Du36cnfp6n_34. Accessed on 12.05.2019.

Committee on Statistics of the Ministry of National Economy of Kazakhstan (2019). Small and GDP Structure Dynamic Tables. Retrieved from http://stat.gov.kz/faces/wcnav_externalId/homeNationalAccountIntegrated?_afrLoop=9558018356663492#%40%3F_afrLoop%3D9558018356663492%26_adf.ctrl-state%3Du36cnfp6n_60. Accessed on 12.05.2019.

Committee on Statistics of the Ministry of National Economy of Kazakhstan (2019). Small and Medium Enterprises. Retrieved from http://stat.gov.kz/faces/wcnav_externalId/homeNumbersSMEnterprises?_afrLoop=9557937601263568#%40%3F_afrLoop%3D9557937601263568%26_adf.ctrl-state%3Du36cnfp6n_47. Accessed on 12.05.2019.

Government.kz (2019). A. Mamin: Kazakhstan’s economy grew by 4%. Retrieved from http://www.government.kz/ru/novosti/1017573-a-mamin-rost-ekonomiki-kazakhstana-sostavil-4.html. Accessed on 18.05.2019.

Kazpravda.kz (2019). The driver of industrialization should be engineering. Retrieved from https://www.kazpravda.kz/news/ekonomika/draiverom-industrializatsii-dolzhno-stat-mashinostroenie–mamin. Accessed on 10.05.2019.

National Bank of Kazakhstan (2019). Credits issued by banks, by type of economic activity (according to extended classification) and interest rates on them. Retrieved from https://nationalbank.kz/?docid=3458&switch=russian. Accessed on 14.05.2019.

Note: The views expressed in this blog are the author’s own and do not necessarily reflect the Institute’s editorial policy.

Kanat Makhanov

Senior Research fellow

Kanat Makhanov is a research fellow at the Eurasian Institute of the International H.A Yassawi Kazakh-Turkish University. He holds a BA in Business Economics from the KIMEP University from 2012. In 2014 he earned his Masters degree in Economics from the University of Vigo (Spain), completing his thesis on “Industrial Specialization in autonomous regions of Spain and Kazakhstan”. His main research interests are Spatial Economics, Economic Geography, Regional Economics, Human and Economic Geography.